All Categories

Featured

Table of Contents

The inquirer stands for a client that was a complainant in an accident matter that the inquirer chosen part of this complainant. The defendants insurer agreed to pay the plaintiff $500,000 in an organized negotiation that requires it to purchase an annuity on which the plaintiff will certainly be detailed as the payee.

The life insurance policy company releasing the annuity is a qualified life insurance policy business in New York State. N.Y. Ins.

N.Y. Ins.

N.Y. Ins. The Division has actually reasoned that an annuitant is the possessor of the basic right approved under an annuity agreement and mentioned that ". NY General Advise Opinion 5-1-96; NY General Counsel Point Of View 6-2-95.

Variable Annuity Calculators

Although the proprietor of the annuity is a Massachusetts firm, the designated beneficiary and payee is a local of New York State. Considering that the above mentioned purpose of Post 77, which is to be liberally interpreted, is to secure payees of annuity agreements, the payee would certainly be shielded by The Life insurance policy Business Warranty Company of New York.

* A prompt annuity will not have an accumulation stage. Variable annuities released by Safety Life Insurance Business (PLICO) Nashville, TN, in all states except New York and in New York by Protective Life & Annuity Insurance Coverage Company (PLAIC), Birmingham, AL.

Retirement Planning And Annuities

Investors ought to very carefully take into consideration the financial investment purposes, risks, fees and expenses of a variable annuity and the underlying financial investment options prior to investing. This and various other details is contained in the prospectuses for a variable annuity and its underlying financial investment options. Programs may be obtained by contacting PLICO at 800.265.1545. life insurance annuity policy. An indexed annuity is not a financial investment in an index, is not a protection or stock exchange financial investment and does not join any kind of supply or equity investments.

The term can be 3 years, 5 years, 10 years or any type of number of years in between. A MYGA works by linking up a swelling sum of cash to permit it to collect rate of interest.

Myga Rates Today

If you select to restore the contract, the rate of interest price might differ from the one you had actually initially agreed to. Because passion prices are set by insurance policy firms that offer annuities, it's crucial to do your research study prior to signing a contract.

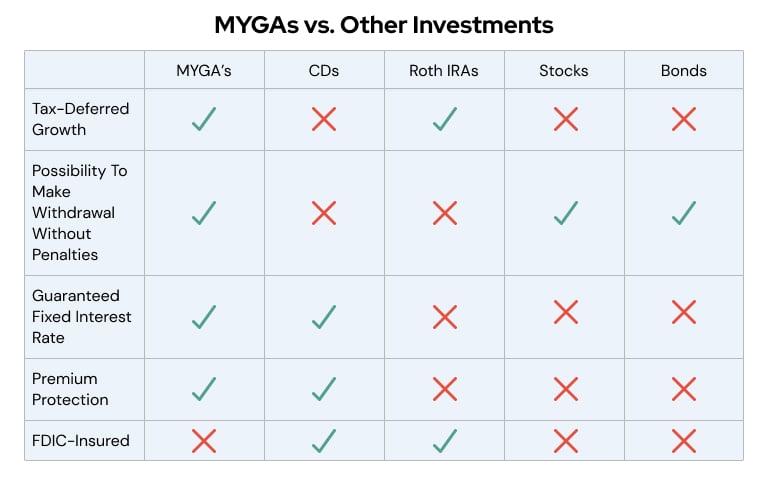

They can defer their tax obligations while still used and not looking for extra gross income. Provided the existing high rate of interest, MYGA has actually ended up being a significant component of retired life economic preparation - america annuity. With the possibility of rates of interest decreases, the fixed-rate nature of MYGA for a set number of years is highly appealing to my customers

MYGA rates are usually greater than CD prices, and they are tax obligation deferred which even more boosts their return. An agreement with more limiting withdrawal stipulations might have higher rates.

They keep occurring. I truly believe that is the finest security you have. Allow's take a look at them in order. In my viewpoint, Claims Paying Capacity of the provider is where you base it. Then you can eye the state warranty fund if you want to, however bear in mind, the annuity mafia is seeing.

They understand that when they place their money in an annuity of any kind, the company is going to back up the insurance claim, and the market is supervising that. Are annuities assured?

If I placed a referral in front of you, I'm additionally putting my certificate on the line. I'm very confident when I put something in front of you when we chat on the phone. That doesn't suggest you have to take it.

Are Annuities Good For Retirement

We have the Claims Paying Ability of the carrier, the state warranty fund, and my friends, that are unknown, that are circling around with the annuity mafia. That's an accurate solution of a person that's been doing it for an extremely, really long time, and that is that a person? Stan The Annuity Male.

People typically get annuities to have a retirement earnings or to build financial savings for an additional purpose. You can purchase an annuity from an accredited life insurance coverage agent, insurance policy business, economic coordinator, or broker. You ought to speak to a monetary consultant regarding your needs and objectives prior to you purchase an annuity.

Safe Annuity

The difference in between the 2 is when annuity repayments start. You don't have to pay taxes on your profits, or payments if your annuity is a specific retired life account (INDIVIDUAL RETIREMENT ACCOUNT), till you take out the earnings.

Deferred and prompt annuities offer a number of options you can pick from. The options offer various degrees of prospective danger and return: are assured to make a minimum rates of interest. They are the most affordable financial danger but provide reduced returns. gain a higher rate of interest, yet there isn't an ensured minimum interest price (7 annuity).

Variable annuities are greater danger since there's a possibility you might lose some or all of your cash. Fixed annuities aren't as dangerous as variable annuities because the financial investment danger is with the insurance policy business, not you.

Average Interest Rate On Annuities

Set annuities assure a minimum passion price, usually in between 1% and 3%. The company may pay a higher passion price than the ensured passion rate.

Index-linked annuities show gains or losses based on returns in indexes. Index-linked annuities are extra complex than dealt with deferred annuities.

Each relies on the index term, which is when the firm computes the interest and credits it to your annuity. The figures out just how much of the increase in the index will certainly be made use of to determine the index-linked interest. Other important attributes of indexed annuities consist of: Some annuities top the index-linked passion rate.

The flooring is the minimal index-linked passion price you will make. Not all annuities have a flooring. All repaired annuities have a minimal guaranteed worth. Some business make use of the standard of an index's worth as opposed to the value of the index on a specified day. The index averaging might happen whenever throughout the regard to the annuity.

Other annuities pay compound rate of interest during a term. Substance passion is rate of interest earned on the cash you conserved and the passion you earn.

Annuities 10

This portion could be utilized rather of or in enhancement to a participation rate. If you secure all your money prior to completion of the term, some annuities will not credit the index-linked passion. Some annuities may attribute just part of the rate of interest. The percent vested generally raises as the term nears completion and is constantly 100% at the end of the term.

This is because you bear the financial investment risk instead of the insurance coverage company. Your representative or monetary advisor can aid you decide whether a variable annuity is right for you. The Securities and Exchange Compensation identifies variable annuities as securities since the efficiency is originated from supplies, bonds, and various other financial investments.

What Are The Best Annuities

Find out a lot more: Retirement in advance? Believe regarding your insurance coverage. (30 year annuity) An annuity agreement has 2 phases: a build-up stage and a payment stage. Your annuity gains interest during the build-up phase. You have numerous choices on just how you add to an annuity, depending upon the annuity you get: enable you to pick the moment and quantity of the settlement.

allow you to make the exact same settlement at the same period, either monthly, quarterly, or every year. The Irs (INTERNAL REVENUE SERVICE) controls the taxes of annuities. The internal revenue service enables you to delay the tax obligation on revenues until you withdraw them. If you withdraw your earnings prior to age 59, you will possibly need to pay a 10% early withdrawal charge along with the taxes you owe on the rate of interest earned.

After the buildup stage finishes, an annuity enters its payment stage. This is sometimes called the annuitization stage. There are a number of alternatives for getting payments from your annuity: Your business pays you a taken care of amount for the time mentioned in the agreement. The company pays to you for as lengthy as you live, however there are not any kind of payments to your beneficiaries after you pass away.

Several annuities bill a fine if you take out money before the payment phase. This penalty, called a surrender cost, is commonly highest possible in the early years of the annuity. The cost is usually a portion of the withdrawn cash, and typically begins at about 10% and goes down every year up until the surrender period is over.

{kind=link}

Table of Contents

Latest Posts

Decoding Fixed Index Annuity Vs Variable Annuities A Closer Look at Fixed Vs Variable Annuity Pros And Cons Defining Variable Annuities Vs Fixed Annuities Advantages and Disadvantages of Annuities Var

Exploring What Is A Variable Annuity Vs A Fixed Annuity Everything You Need to Know About Financial Strategies Breaking Down the Basics of Investment Plans Features of Smart Investment Choices Why Fix

Highlighting the Key Features of Long-Term Investments A Comprehensive Guide to Investment Choices Breaking Down the Basics of Variable Annuity Vs Fixed Indexed Annuity Advantages and Disadvantages of

More

Latest Posts